Bitcoin Core Development

Public Blockchains and Regulated Financial Institutions with JPMC

Stablecoins in Africa: Translating Global Principles into Local Regulatory Practice

Coin selection by Random Draw according to the Boltzmann distribution

The Hidden Plumbing of Stablecoins: Financial and Technological Risks in the GENIUS Act Era

Bitcoin Kernel API

Bitcoin Core Peer-to-Peer Process Isolation

Designing Payment Tokens For Safety, Integrity, Interoperability, and Usability with JPMC

Improving Bitcoin-Core’s Kitchen Sink Random Number Generator

Privacy Preserving Designs for CBDCs with Deutsche Bundesbank

51% Attacks

ADESS: a proof of work blockchain protocol modification to deter double-spend attacks

An Empirical Analysis of Chain Reorganizations and Double-Spend Attacks on Proof-of-Work Cryptocurr

Application of Programmability to Commercial Banking and Payments with JPMC

Auditable Private Ledgers - Student Thesis

AUDIT: Practical Accountability of Secret Processes

Beware the Weak Sentinel: Making OpenCBDC Auditable without Compromising Privacy

b_verify: Supply Chain Records

b_verify: Scalable Non-Equivocation for Verifiable Management of Data - Student Thesis

CBDC as a cryptographic platform with the Bank of Canada

CBDC: Expanding Financial Inclusion or Deepening the Divide

ClockWork: An Exchange Protocol for Proofs of Non Front-Running

Compelled Decryption and the Fifth Amendment: Exploring the Technical Boundaries

Cryptanalysis of Curl-P and Other Attacks on the IOTA Cryptocurrency

Cryptoeconomic Systems Journal

Cryptokernel | A Blockchain Toolkit

Discreet Log Contracts

Double-Spend Counterattacks: Threat of Retaliation in Proof-of-Work Systems

Enhancing the Privacy of a Digital Pound with Bank of England

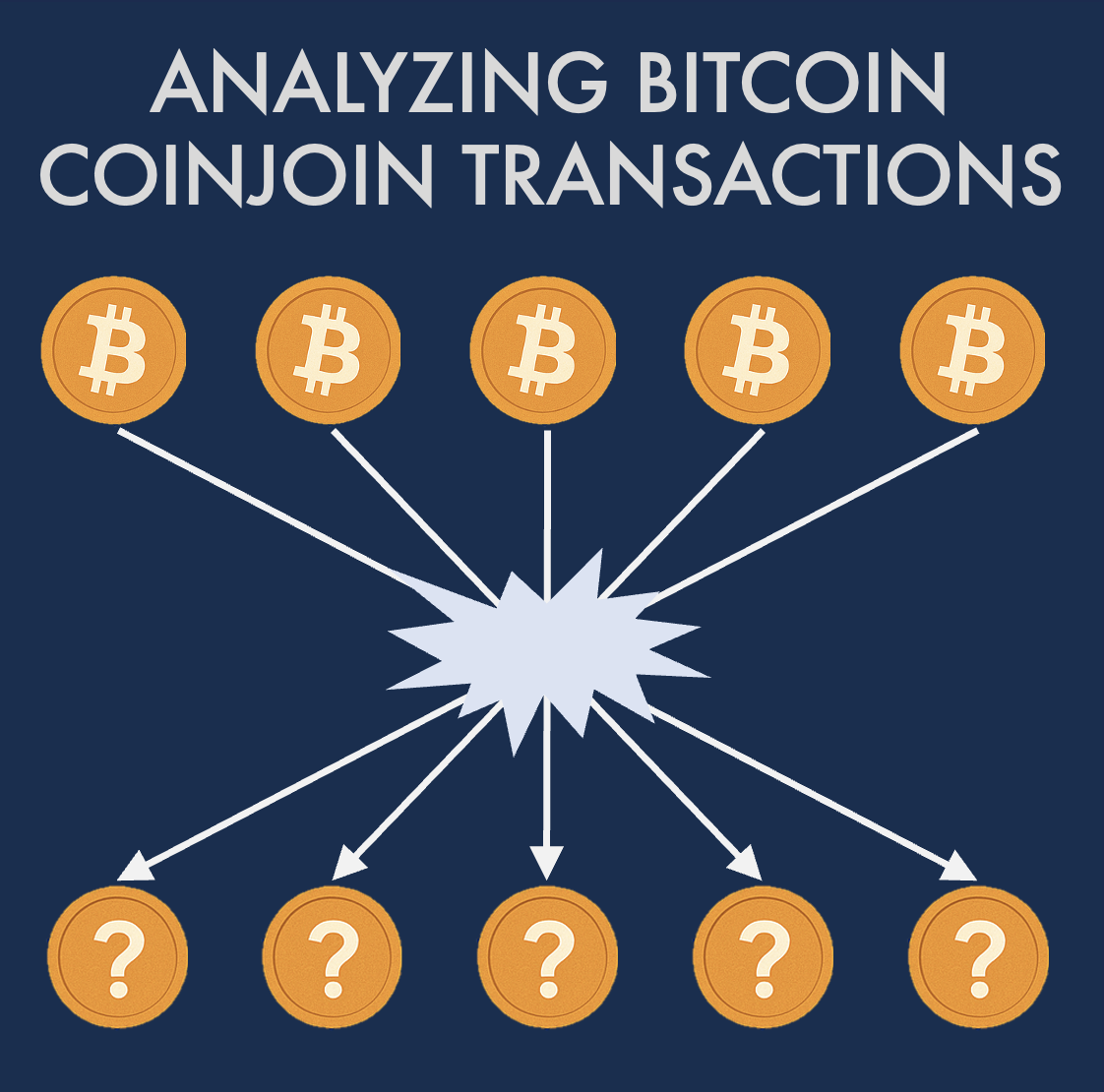

Evaluating the Practical Privacy of Whirlpool Coinjoins

Going from bad to worse: from Internet voting to blockchain voting

It wasn't me! Repudiability and Unclaimability of Ring Signatures

Mitigating Undercutting Attacks: A Study on Mining and Transaction Fee Behavior - Student Thesis

Opensolar

Parallelized Architecture for Scalably Executing Smart Contracts (PArSEC)

Pool Detective | Mining Pool Monitoring

Privacy-preserving analytics for the securitization market: a zero-knowledge distributed ledger tech

Project Hamilton and OpenCBDC

Responsible Vulnerability Disclosures in Cryptocurrencies

Scaling Privacy Preserving Payments - Student Thesis

SpaceMint: A Cryptocurrency Based on Proofs of Space

Static-Memory-Hard Functions, and Modeling the Cost of Space vs. Time

Targeted Nakamoto: A Bitcoin Protocol to Balance Network Security and Energy Consumption

The Decentralized Web: Defending Internet Freedom through Decentralization: Back to the Future?

The Future of Our Money: Centering Users in the Design of Digital Currency

The Impact of Blockchain Technology on Finance: A Catalyst for Change

The Lightning Network Cross-Chain Exchange: A Decentralized Approach for Peer to Peer Exchange

Transformable Discreet Log Contracts - Student Thesis

Utreexo

Verifiably Delaying Adversaries in Consensus

ZK Ledger | The Future of Audit

zk-SHARKS | zero-knowledge Succinct Hybrid Arguments of Knowledge

Blockchain Labs - Reports 2018

Blockchain Labs - Reports 2019

Blockchain Labs - Reports 2020